FTSE 100 FINISH LINE 5/5/26

FTSE 100 FINISH LINE 5/5/26

London’s FTSE 100 traded sharply lower on Tuesday, May 5, sliding around 1% as a weak response to HSBC’s results and another surge in oil prices weighed on sentiment. The move stood out because broader European equities were firmer, with regional markets taking support from upbeat earnings, while London underperformed. That divergence reinforced the same theme seen over recent sessions: the FTSE is still highly sensitive to its heavyweight financials and to the inflationary implications of higher energy prices, even when other global markets are finding reasons to rally.

The key single-stock pressure point was HSBC, whose update disappointed investors and dragged on the banking complex. In a market already focused on the Bank of England’s cautious stance and the risk that sticky inflation delays easier policy, any weakness from a major lender carries outsized index weight. The issue was not simply one bank’s earnings; it was what the reaction said about investor tolerance. After several weeks of geopolitical stress, higher oil, and uncertainty over rates, the market is still quick to punish any large-cap update that fails to deliver a clean beat or a confident outlook.

Oil was the other major driver. Crude’s latest spike, linked to renewed U.S.-Iran tensions, was not treated as an uncomplicated positive for the FTSE, despite the index’s exposure to energy majors. Instead, investors focused on the broader macro cost: higher fuel prices, renewed inflation pressure, and the risk that UK consumers and businesses face another squeeze. That matters more for London than for some peers because the UK economy remains especially exposed to energy-price shocks. The result was a familiar split: energy names may receive some earnings support, but the index as a whole struggles when higher oil starts to look like a tax on growth rather than a sector tailwind.

The broader market message was therefore defensive. While global stocks found support from stronger corporate earnings and European shares generally moved higher, the FTSE 100 lagged because its own mix of bank disappointment, oil-driven inflation risk and domestic vulnerability kept buyers cautious. After last week’s Bank of England hold, investors remain alert to any sign that energy prices could force policymakers into a less dovish path. Sterling, gilt yields and UK cyclicals are all effectively trading around the same question: whether the next phase of the Middle East shock is disinflationary through weaker growth, or inflationary through sustained commodity pressure.

Politically, the backdrop remains uncomfortable for Prime Minister Keir Starmer’s government. The market is not trading Westminster headlines tick-for-tick, but the combination of energy insecurity, cost-of-living sensitivity and fragile confidence keeps UK risk premia alive. For the FTSE, Tuesday’s decline was not a panic move, but it was a meaningful warning: London can still lag even when global equities are firm if heavyweight earnings disappoint and oil moves from being a profit driver to a macro threat. The finish line is clear: May 5 was a “bad mix” session — HSBC hurt the index, oil hurt the macro story, and the FTSE’s sector structure failed to provide enough offset

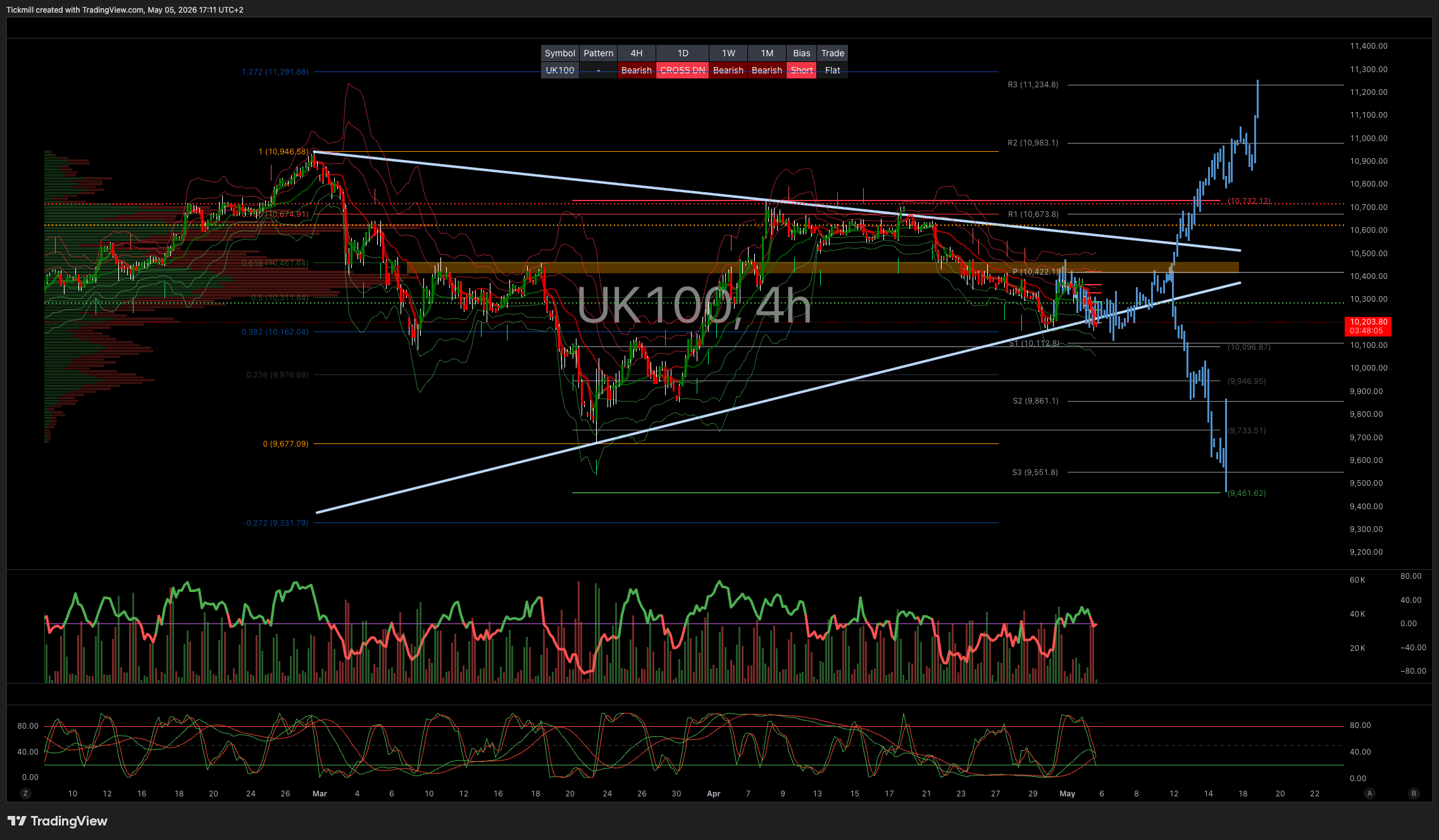

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bearish

Weekly VWAP Bearish

Above 10500 Target 11000

Below 10100 Target 9469

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!