S&P500 Trading Update 29/4/26

S&P500 Trading Update 29/4/26

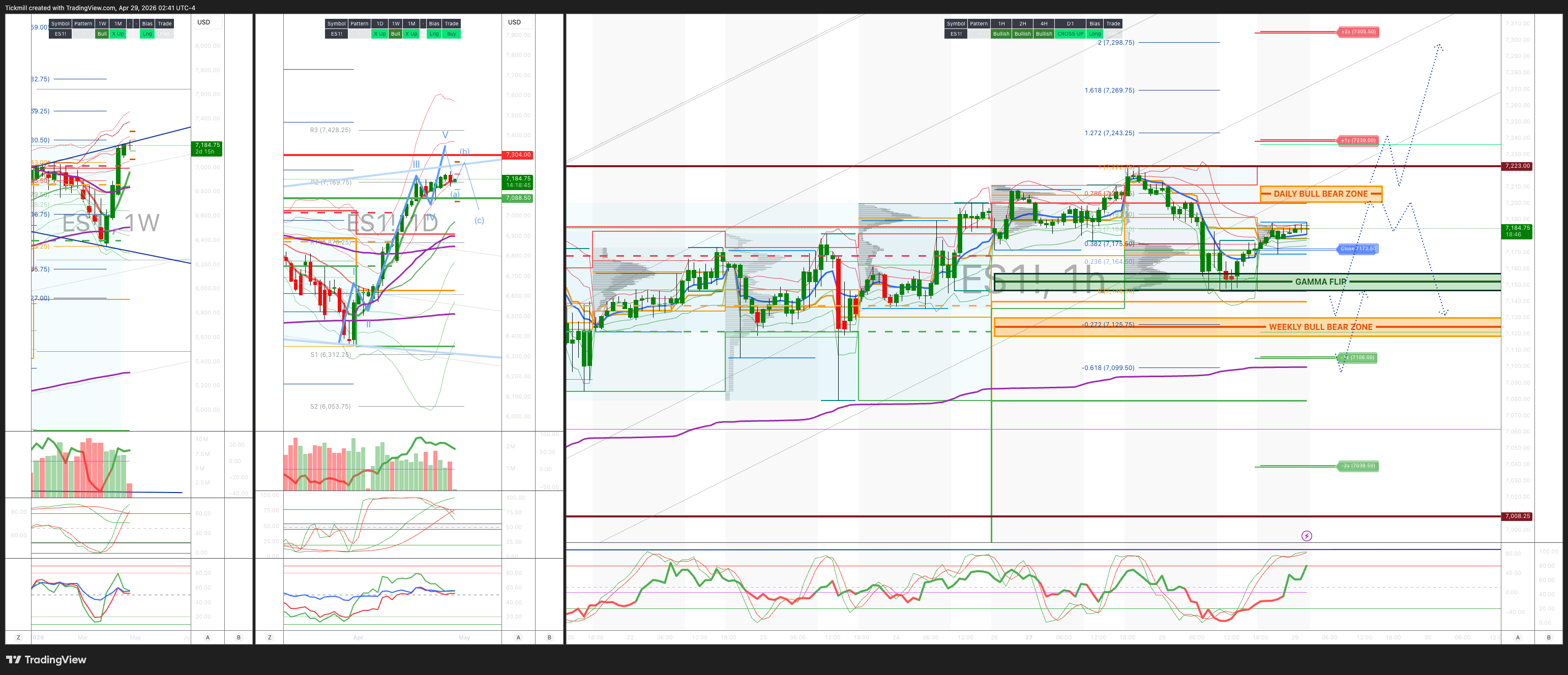

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7130/20

WEEKLY RANGE RES 7304 SUP 7087

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.18 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7174

WEEKLY VWAP BULLISH 6819

MONTHLY VWAP BULLISH 6815

DAILY STRUCTURE – BALANCE - 7211/7079

WEEKLY STRUCTURE – OTFH - 7079

MONTHLY STRUCTURE - BALANCE

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7200/10

GAMMA FLIP 7151

DELTA FLIP 6881

DAILY RANGE RES 7239 SUP 7106

2 SIGMA RES 7305SUP 7039

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

SHORT ON REJECT/RECLAIM OF DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

LONG ON RACCEPTANCE ABOVE DAILY BULL BEAR ZONE TARGET DAILY > WEEKLY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘MO WOBBLE’

US equities finished lower in a choppy but orderly session, with the S&P 500 -49bps to 7,139, NDX -101bps to 27,029, R2K -115bps to 2,756, and the Dow nearly flat at -5bps to 49,142. Volumes remained subdued at 15.5bn shares across US exchanges versus a 19.4bn YTD daily average, reinforcing the sense that investors are still reluctant to make large directional commitments ahead of the megacap earnings/FOMC catalyst stack. The close saw a $1.9bn MOC buy imbalance, but it was not enough to meaningfully change the tone.

Macro cross-asset signals were mixed. WTI crude rallied 3.4% to $99.64 on the continued absence of concrete Middle East de-escalation and headlines around the UAE/OPEC+ framework, keeping the energy shock front and center. 10Y yields were unchanged at 4.34%, DXY firmed 15bps to 98.65, gold fell 1.8% to $4,598, and Bitcoin slipped 80bps to $76,350. Notably, VIX fell 1.17 vols to 17.81 despite the equity selloff, consistent with an orderly de-risking rather than a disorderly hedge scramble.

Tape Tone — Momentum Hit, But No Broad Panic

The main damage came in momentum, which fell 7% following reports that OpenAI is missing sales targets. That marked one of the worst days for the factor pair in the past five years — a 99th percentile move — and fully unwound what had previously been the strongest ten-day momentum gain on record. The move mattered because the tape is still heavily dependent on “generals” to define risk appetite into May.

Single-stock activity was relatively tame despite the factor stress. Floor activity was around 5/10, with asset managers finishing roughly $1.5bn net sellers, led by broad supply across discretionary, healthcare, materials and industrials. Hedge fund flows skewed modestly for sale, though no single sector stood out as a major source of pressure.

Derivatives — Spot Down, Vol Down

The options market sent a relatively benign signal. Despite the selloff, the desk saw spot down / vol down for much of the session, with vols relaxing across the curve. That likely reflects the market moving into areas of longer dealer gamma and the presence of downside dealer gamma supply, which helped dampen realized volatility.

Importantly, the market had already out-realized the daily straddle-implied move within the first hour, yet the rest of the session remained orderly. Hedges were rolled up and out rather than aggressively added. The straddle into tomorrow’s FOMC plus megacap earnings finished implying a 0.57% S&P move. The vol desk preference is upside in META/AMZN and downside in AAPL/GOOGL.

Post-Close Earnings

SBUX +4%: Expectations were elevated, but results cleared the bar. Comps were roughly in line, while better EPS appears to be driving the positive reaction.

BKNG -8%: Room nights missed, with management citing macro and Middle East headwinds; shares are nearly back to YTD lows.

STX +10%: Strong beat and June-quarter revenue guide implying +11% q/q growth.

BE +8%: Top- and bottom-line beat.

EIX -1.5%: Q1 EPS ahead, but revenue missed.

HOOD -6%: Slight EPS miss, driven by revenue downside, partly offset by better expenses.

TER -8%: Q1 revenue and EPS beat, but the stock is now roughly 18% below last Friday’s ATH close, suggesting expectations had become stretched.

Megacap Earnings Setup

The next 48 hours are pivotal. GOOGL, MSFT, AMZN and META report Wednesday post-close, representing roughly 17.5% of the S&P 500, followed by AAPL on Thursday, another 6% index weight. The setup is delicate: megacap tech moved from technically oversold to overbought in just 13 trading sessions, with the 14-day RSI for the basket moving from below 30 on March 30 to 74 by April 17.

GOOGL

Positioning: 9.5/10. The stock remains very well owned, though the pace of incremental inflows has slowed. Expectations have drifted higher. Investors now expect GCP growth in the high-50s to 60% range, versus Street expectations closer to the mid-50s, while Search is expected in the high teens versus GIR at 17.5%. Capex commentary is expected to be reiterated. Options imply a 5% move.

AMZN

Positioning: 8.5/10. Positioning has moved higher recently after a wave of inflows. The AWS bogey has also risen, with investors now looking for something closer to 30%+ growth, versus GIR at 26% y/y. Commentary on Trainium, AI partnerships and the durability of AWS acceleration will be key. Options imply a 7% move.

META

Positioning: 7.5/10. Sentiment has improved off a lower base, helped by the MuseSpark release and evidence of more tangible progress around AI. The key focus areas are opex clarity, evidence of operating leverage, and the 2Q ads outlook, particularly the scale of any deceleration. Options imply a 6.5% move.

MSFT

Positioning: 5.5/10. There has been some recent buying, though it feels more like risk-management covering of underweights than a clean long build. Sentiment remains notably bearish, especially among hedge funds. For Azure, investors expect stable growth in the quarter and guide, around the high-30s y/y constant currency area. Copilot/M365 traction and capex commentary, especially the FY27 trajectory, will be central. Options imply a 6.5% move.

AAPL

Positioning: 7/10. Investor apathy remains elevated, with Apple largely sitting outside the core AI trade and trading with more defensive characteristics. Options imply only a 3% move, much lower than the other megacap reporters. Strength is expected from Services, with growth around 13–14% y/y, and continued momentum from the iPhone 17 cycle. Investors will focus on component costs, China recovery, Apple Intelligence and any CEO-transition commentary.

Bottom Line

This was not a panic selloff, but it was a meaningful warning shot. Momentum cracked hard, oil is again pressuring the macro narrative, and investors are waiting for megacap earnings to either validate or challenge the recent risk-on rebound. With positioning no longer washed out and volatility subdued, the hurdle for earnings is high — especially in the most crowded names. The tape can still work higher, but from here it needs confirmation from the generals.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!