S&P500 Trading Update 8/5/26

S&P500 Trading Update 8/5/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

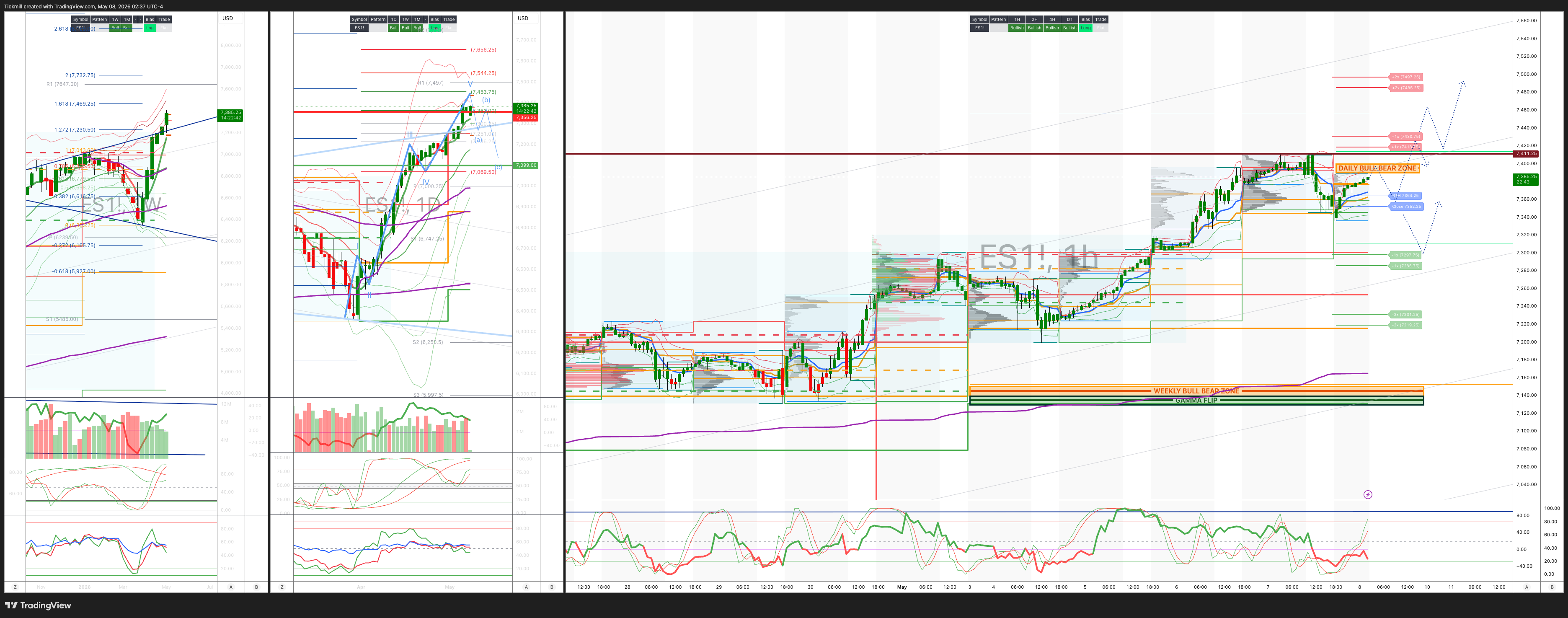

WEEKLY BULL BEAR ZONE 7150/40

WEEKLY RANGE RES 7356 SUP 7138

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.21 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7322

WEEKLY VWAP BULLISH 7118

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFH - 7345

WEEKLY STRUCTURE – OTFH - 7137

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7390/7400

GAMMA FLIP 7135

DELTA FLIP 6950

DAILY RANGE RES 7418 SUP 7286

2 SIGMA RES 7497 SUP 7231

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

SHORT ON TEST/REJECT DAILY BULL BEAR ZONE TARGET DAILY RANGE SUP

LONG ON ACCESPTANCE ABOVE DAILY BULL BEAR ZONE TARGET GAILY RANGE RES > 7450/60

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Unwindy’

US equities paused after the prior melt-up, with the S&P -38bps to 7,337, NDX -12bps to 28,564, R2K -163bps to 2,840, and Dow -63bps to 49,597, despite a sizable +$3.8bn MOC buy imbalance. Volumes remained healthy at 19.3bn shares, slightly above the 19bn YTD average. Cross-asset was mixed rather than outright hostile: WTI +98bps to $96.02, 10Y +3bps to 4.38%, DXY +14bps to 98.16, gold +41bps to $4,711, Bitcoin -160bps to $80,118, while VIX fell -178bps to 17.08. The headline index move was modest, but the factor move was not: High Beta Momentum fell 8%, a top-ten one-day move in the pair over the past five years, with five of those instances now occurring in 2026. That was driven by unwindy price action on both legs: better software earnings forced a squeeze in prior shorts, with DDOG +31%, FTNT +20%, and DASH +2%, while the AI/semi complex consolidated after a roughly 50% rally since early April, with ARM -10% on sluggish smartphone royalty results, COHR -8% on softer gross margins, and memory taking a breather.

The bigger message is that the market is shifting from “AI melt-up” to “factor digestion.” The fundamental semi/AI story has not broken, especially after the AMD-driven reset earlier in the week, but optimism may be close to tactical capitulation after a huge run and with the bulk of earnings season now behind us. Recent sessions saw a major pickup in high-touch activity across semis, including signs of long-only “stop-ins” into AI infrastructure. That does not mean the top is in, but these bursts of client activity often coincide with either peak fear or peak exuberance. Positioning also argues for more care: momentum exposure in the prime book is at extremes — 99th percentile on a 1-year basis and 100th percentile on a 5-year basis — while valuations are stretched, factor volatility remains elevated, and dispersion is likely to stay high under the surface. The right read is not “sell AI,” but rather stop chasing the entire basket blindly; the next phase should reward stock selection, earnings quality and cleaner risk/reward entries.

Flows were orderly but less supportive. Floor activity was 6/10, finishing -2% for sale versus a 30-day average of +121bps. Asset managers were roughly flat, while hedge funds were slight net sellers, with no major sector skew standing out. Two IPOs priced/traded, SUJA and HAWK, but single-stock activity remained controlled. Consumer was the weak spot from a fundamental read-through perspective, with disappointing restaurant commentary from SHAK, BROS and CAVA. That said, sellers remain hesitant because of the risk of a larger Iran deal and another leg lower in oil. With limited seller appetite but also little generalist interest, activity in consumer has faded even as single-name moves remain large in both directions. In other words, consumer remains a positioning squeeze candidate if crude keeps falling, but the earnings commentary is not yet strong enough to attract broad-based new sponsorship.

Derivatives confirmed the shift from panic hedging to selective event trading. Spot and vol both traded lower, with SPX vol offered across the curve and index flows relatively quiet. Skew caught a small bid in the front end but was little changed further out. NDX and RUT vol were similarly offered, though front-end skew was better bid. The most notable demand was for software upside after the squeeze, especially IGV call spreads out to June/July. There was also single-name micro demand in MSFT, including a buyer of the Nov 500/575 call spread in roughly 26k and a buyer of the Dec 475/525 call ratio. The market is still willing to pay for upside optionality in software and mega-cap quality, but broad index vol is being sold as realized cools and dealers remain comfortable. Ahead of NFP at 8:30am ET and UMich sentiment at 10am ET, the implied move through Friday is 58bps, so the bar for a meaningful macro shock is not especially high.

After-hours earnings kept the dispersion theme alive. AKAM +20% was the standout after saying a leading frontier model provider committed to $1.8bn over seven years for CIS, giving the market a fresh AI infrastructure monetization angle. IREN +18% rallied on NVDA investment, and MCHP +5% beat and guided above. On the negative side, NET -16% was hit despite trading near all-time highs and entering the print at a mid-20s EV/sales multiple, showing how unforgiving the tape remains for expensive growth. HUBS -11% fell despite a headline beat/guide above, TOST -9% guided down on 2Q EBITDA, EXPE -4% had a solid 1Q EBITDA beat but room-night deceleration, and ABNB -2% slipped despite a beat/raise. The theme is clear: high multiple stocks need not just beats, but clean acceleration, margin confidence and no cracks in forward indicators.

The macro focus now shifts to payrolls. The NFP estimate is +75k for April, with unemployment expected unchanged on a rounded basis at 4.3%, though the bar for a round-down to 4.2% is low given the prior unrounded 4.26%. Average hourly earnings are expected at +0.3% m/m, with neutral calendar effects. The positives are solid big-data job indicators and still-low high-frequency layoff measures. The negatives are expected government payroll weakness, including a 10k decline in federal jobs partly offset by +5k state/local, leaving total government payrolls down around 5k. A soft-but-not-ugly print would probably be equity-friendly if it keeps yields contained without raising recession concerns. A hot wages/yields print is the bigger risk for crowded momentum and long-duration growth.

Trading takeaway: this was not a broad risk-off day; it was a crowded factor unwind. The AI/semi trade is consolidating after an extreme move, while software is squeezing on better earnings and improved positioning. Stay constructive on secular AI infrastructure, but stop chasing extended baskets after 50% moves and use rallies to trim the most crowded momentum exposure. Prefer cleaner expressions: long software/quality growth with earnings support, selective AI infrastructure names with real revenue conversion, and call spreads rather than outright spot-chasing in semis. Consumer remains a tactical squeeze if oil keeps falling, but weak restaurant commentary argues against broad fundamental conviction. Into NFP, the key is yields: if payrolls are soft enough to keep the 10Y contained, dips can still be bought; if wages/yields re-accelerate, crowded momentum remains the pressure point.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!